Cannacurio #120: Cultivation license summary Q3 2025

The cannabis supply chain begins in the cultivation space and cultivation activity remains one of the most reliable indicators of where markets are headed. Plant count, canopy size and licensing speed all show how each state balances supply, demand and regulatory pressures.

Growing licenses continued to cool in the third quarter of 2025 as states faced oversupply and reassessed their capacity. A number of key markets slowed or paused issuance, while a handful of emerging markets continued to grow.

Important insights into cultivation

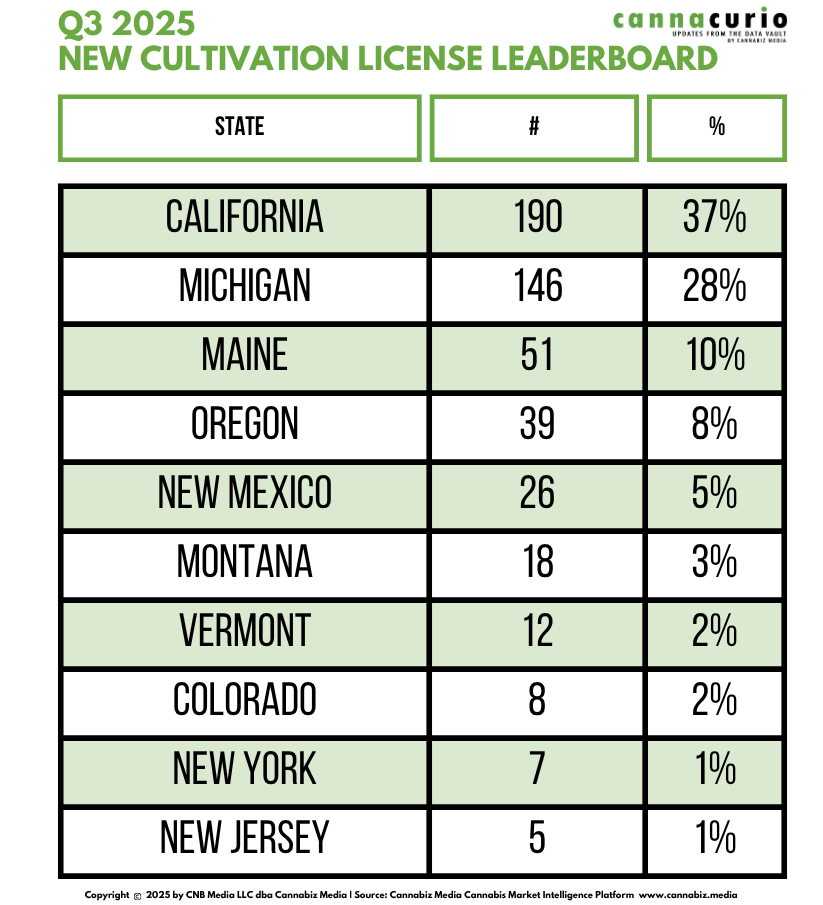

- 518 cultivation licenses were issued in the third quarterstrongly downward from 729 in the second quarter.

- California carried edition with 190 licenses (37%),followed by Michigan (146) And Maine (51).

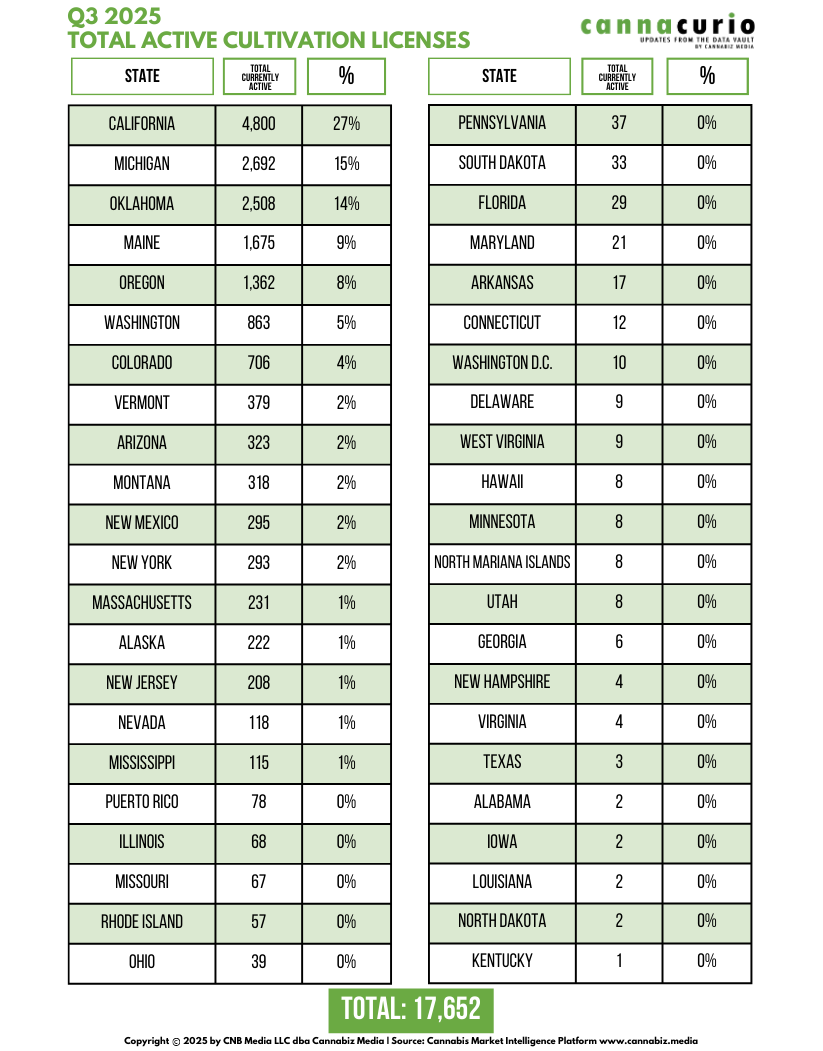

- The US has now done it 17,652 active cultivation licensesa decrease of 18,164 at the end of Q2.

- Licensing has remained relatively stable over the last 12 months –with the exception of Aprilas Michigan added 210 new licenses in a single month.

Last year showed moderate, consistent activity with one clear outlier: Michigan's April surge. Beyond that increase, states appear to be settling into a slower, more cautious licensing pace as oversupply weighs on producers' economies.

Q3 2025 Cultivation Rankings

California remains at the top of the rankings, but Michigan's continued licensing activity has resulted in a two-state race in overall licensing. Maine's presence in the top three highlights the steady production of smaller but active markets.

In the first nine months of 2025, the top emitting states reflect a mix of mature markets, states still building out their infrastructure, and newer entrants expanding their capacity.

Active License Concentration: Key States

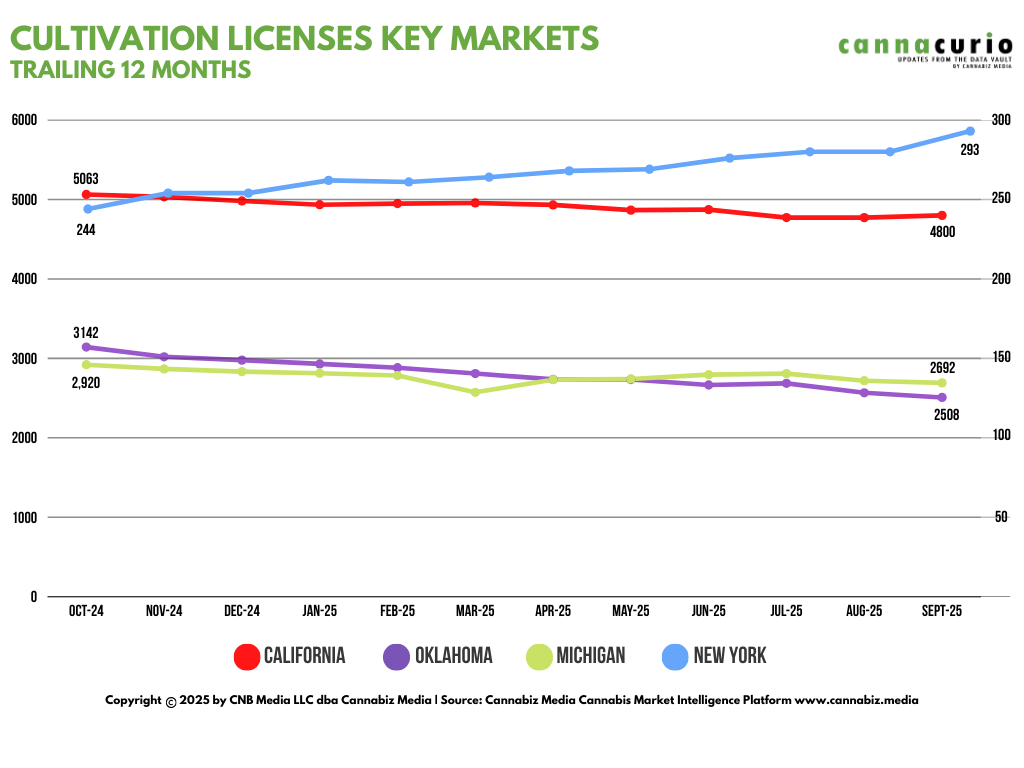

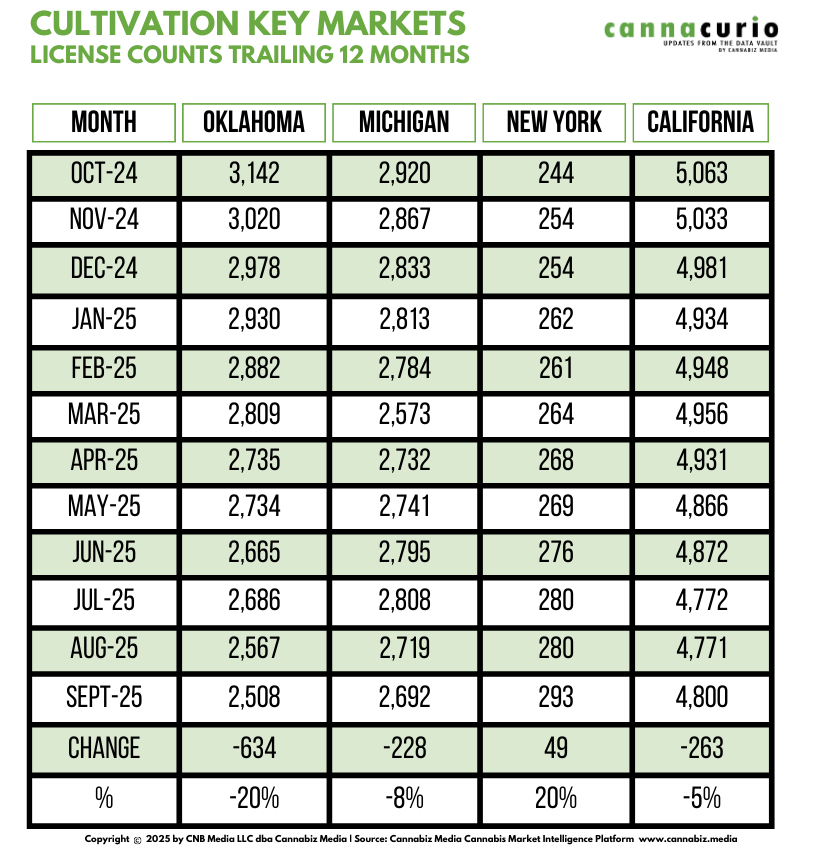

The chart below shows the total number of active licenses for Oklahoma, Michigan, California and New York. New York is the only market where the number of cultivation licenses is growing. The Empire State is up 20% while Oklahoma is down 20%.

A comparison of the total active cultivation licenses in Oklahoma, Michigan, California and New York shows different developments:

- new York is the only state in the group where cultivation licenses are going up, and up 20%the course of the year so far.

- Oklahoma continues its sharp decline, downwards 20% after years of oversupply and over-licensing.

- California And Michigan remain large-volume markets, but are no longer expanding in a meaningful way.

- The monthly tables reinforce this divide between states that are tightening supply and those that are still building supply.

National View: Total number of active cultivation licenses

California still has the largest number of cultivation licenses in the country. Michigan's steady growth has allowed it to overtake Oklahoma, reflecting a shift in the national hierarchy.

But what unites all three markets – despite their differences in size – is: Oversupply. Every state is grappling with too much canopy cover and inconsistent demand growth, prompting regulators to reevaluate how much new production the market can sustain.

Diploma

The third quarter reinforced the shift toward stricter supply management across the country. California maintains its lead in cultivation licenses, but this quarter isn't about which state comes out on top – it's about the growing number of states putting on the brakes.

As wholesale prices remain under pressure, regulators are taking action Montana, OregonAnd Oklahoma have issued moratoriums on new cultivation licenses. Massachusetts is currently considering similar steps, either through a formal pause on new cultivation licenses or by reducing the amount of canopy allowed.

These steps signal a broader transition to one Managed care erawhere states play a more active role in preventing destabilizing oversupply. In the meantime, New York's further expansion is one of the few bright spots for farmers, although increases in production will also ultimately test the balance of this market.

Key factors to keep an eye on in the fourth quarter include:

- Whether Michigan's aggressive licensing is cooling off

- How quickly New York's 20 percent year-to-date growth is translating into market activity

- Other states are considering moratoriums or canopy adjustments

- The pace of consolidation and license loss in oversupplied markets

- How strictly will Minnesota manage the rollout of its new license?

The cultivation landscape remains dynamic, but the direction is becoming increasingly clear: Many countries prioritize stability over expansion.

author

Ed Keating is co-founder of Cannabiz Media and oversees the company's data research and government relations. Throughout his career, he has worked with and advised information companies in the compliance area. Ed has led product, marketing and sales while overseeing complex, multi-country product lines in the securities, corporate, UCC, security, environmental and human resources markets.

At Cannabiz Media, Ed enjoys the challenge of working with regulators around the world as he and his team collect corporate, financial and licensing information to track the people, products and companies in the cannabis economy.

Ed graduated from Hamilton College and received his MBA from the Kellogg School of Northwestern University.

Cannabiz Media customers can stay up to date on these and other new licenses through our newsletter, alerts and reporting modules. Subscribe to our newsletter to receive these weekly reports straight to your inbox. Or you can schedule a demo to get more information about how you can access Cannabiz Media's Cannabis Market Intelligence platform yourself and dive deeper into this data.

Cannacurio is a regular column from Cannabiz Media featuring insights from the most comprehensive licensing data platform. Check out Cannacurio posts and podcasts for the latest updates and information.

Post a comment: